Lawyer Than Trong Ly – Le Thi Dung – Le Thi An

Issuing corporate bonds is a popular method of raising capital for enterprise, especially for the real estate companies. The private placement of corporate bonds in Vietnam is currently a hot topic in the mass media in the context of tightening credit and bond markets. It leads to many difficulty, whereby many individuals and real estate companies were prosecuted for criminal liability following the event that several bond lots issued by affiliate members of Tan Hoang Minh Group were canceled by state authority due to violating regulations on issuing corporate bond.

Currently issuing corporate bonds is governed directly by Decree 153/2020/ND-CP of the Government dated 31 December 2020, adjusted and amended by Decree 65/2022/ND-CP effective from 16 September 2022 (“Decree 65/2022”). In order to help readers understand more about this issue, we hereby summarize the current regulations on order, procedures and conditions for private placement of bonds in the Vietnamese market, thereby raising awareness of legal compliance and minimizing risks for businesses.

1. The understanding of corporate bonds

a. Definition

Corporate bonds are bonds issued by enterprise, in the form of certificates or debit notes. For this type of bond, the issuer is obliged to pay both principal and interest to the bondholder when it comes due. Thus, bondholders are creditors of the bond issuers. Normally, the purpose of issuing bonds is to raise capital to expand production, business, invest in development or restructure debt on the principle of self-borrowing, self-paying, self-responsibility for the efficiency of capital use and ensure the debt repayment ability of the enterprise.

b. The type of corporate bonds

Currently, on the market, corporate bonds are classified into two types: (i) listed bonds; and (ii) over-the-counter bonds.

Accordingly, listed bonds are bonds that are fully registered and deposited at the Securities Depository Center. This type of bonds are issued to the public on centralized stock exchanges (HNX and HSX), subject to a strict control and monitoring by authorities as well as stock exchanges. Therefore, this type of bond can be conveniently traded by organizations and individuals without restrictions.

Over-the-counter (OTC) bonds are bonds that are not subject to strict regulatory policies like listed bonds, and are traded depending on the needs of the parties. This bond is issued privately and is exchanged on the OTC market.

However, as the conditions for enterprise to issue private bonds are quite easy, in recent years, the number of businesses choosing the form of private bond issuance accounts for a relatively high proportion compared to the method of issuing bonds to the public. This requires investors to have the knowledge, ability to understand, analyze and evaluate the market to select bonds that are profitable and less risky.

In addition, based on the nature of corporate bonds, they can be classified into convertible bonds, bonds with warrants, non-convertible bonds without warrants and green corporate bonds. In which, (i) Convertible bond is a type of bond issued by a joint-stock company, which can be converted into ordinary shares of the issuing enterprise under terms and conditions determined in the bond issuance plan; (ii) Bond with warrants is a type of bond issued by a joint-stock company with warrants, allowing its holder to purchase a number of common shares of the issuing enterprise under the terms and conditions as determined in the bond issuance plan; and (iii) Green corporate bonds are corporate bonds issued to invest in projects in the field of environmental protection and projects that are beneficial for the environment in accordance with the law on environmental protection.

2. Subjects and conditions for the private placement of corporate bonds

a. Subjects of the private placement of the bonds in the domestic market are bond issuers, including joint stock companies and limited liability companies established and operating under Vietnamese law and meeting the conditions for issuing corporate bonds as specified in section 2.c below.

b. Objects eligible to buy corporate bonds

i. For non-convertible bonds without warrants, buyers are professional investors (the “Investors”) of securities in accordance with the securities law.

ii. For convertible bonds and bonds with warrants, buyers are professional securities investors and strategic investors, in which the number of strategic investors must be less than 100 investors.

Accordingly, strategic investor is an investor selected by the General Meeting of Shareholders according to the criteria of financial capacity, technology level and has committed to cooperate with the company for at least 3 years[1], and professional securities investors are investors with financial capacity or professional qualifications in securities, including: (i) Commercial banks, foreign branch banks (FBB), finance companies, insurers, securities companies, fund management companies, securities investment funds, international financial institutions, off-budget financial funds, state-owned financial institutions permitted to buy securities as prescribed by relevant laws; (ii) Any company whose contributed charter capital exceeds 100 billion VND; every listed or registered organization; (iii) Holders of securities professional certifications; (iv) Any individual holding a quantity of listed or registered securities that is worth at least 02 billion VND as confirmed by the securities company; (v) Any individual whose taxable income in the latest year is at least 01 billion according to his/her submitted tax return or tax deduction documents of his/her income payer.[2]

In general, private placement of bonds is a “playing field” for strategic investors to limit the participation of inexperienced, and unknowledgeable investors. In fact, there are many amateur individual investors who have circumvented this regulation to invest in bonds through different ways such as borrowing to have a portfolio of two (2) billion dong in a few days, or invest through a capital contribution contract to become a professional investor.

Therefore, in order to administrate the bond market towards sustainable and stable development, Decree 65/2022 has forced professional securities investors to ensure holding portfolios with an average value of two (2) billion VND or more, for a minimum of 180 days, in assets excluding loans. In addition, professional investors are not allowed to sell or contribute capital to invest in bonds with investors who are not professional securities investors in any form to improve transaction quality, ensure the “play field” of professional investors. Furthermore, to limit the access of unprofessional investors when buying corporate bonds, this Decree increases the par value of corporate bonds upon issuance to 100 million VND/bond or a multiple of 100 million dong instead of 100 thousand dong and a multiple of 100 thousand dong as before.

c. Conditions for the private placement of corporate bonds

i. For the offering of non-convertible bonds without warrants (excluding the offering of bonds by a securities company or a securities investment fund management company that is not a public company), the enterprise must meet the following conditions[3]:

1. Be a joint stock company or a limited liability company established and operating under the laws of Vietnam;

2. Full payment of both principal and interest of issued bonds or full payment of due debts for 03 consecutive years before the bond issuance (if any), except for the case of offering bonds to creditors who are selected financial institutions;

3. Satisfy financial safety ratios and operational safety ratios in accordance with specialized laws;

4. Have an approved bond issuance plan;

5. Having a financial statement of the year immediately preceding the year of issuance which is audited by a qualified auditing organization as prescribed in this Decree; and

6. Buyers of the bonds are professional securities investors in accordance with the securities law.

ii. For the offering of non-convertible bonds without warrants by a securities company or a securities investment fund management company that is not a public company, the enterprise must satisfy the conditions specified in section (1), (3), (4), (5) and (6) above[4].

iii. For the offering of convertible bonds or bonds with warrants, the issuing enterprise is a joint-stock company that meets the conditions for the offering specified in section (2), (3), (4) and (5) above, at the same time, buyers shall be professional investors, strategic investors, in which the number of strategic investors must be less than 100. In addition, each batch of offering of such bonds must be separated by at least 06 months from the date of completion of the latest offering, and the conversion of bonds into shares and the exercise of warrants must meet the regulations on the percentage of foreign investors’ ownership as prescribed by law.[5]

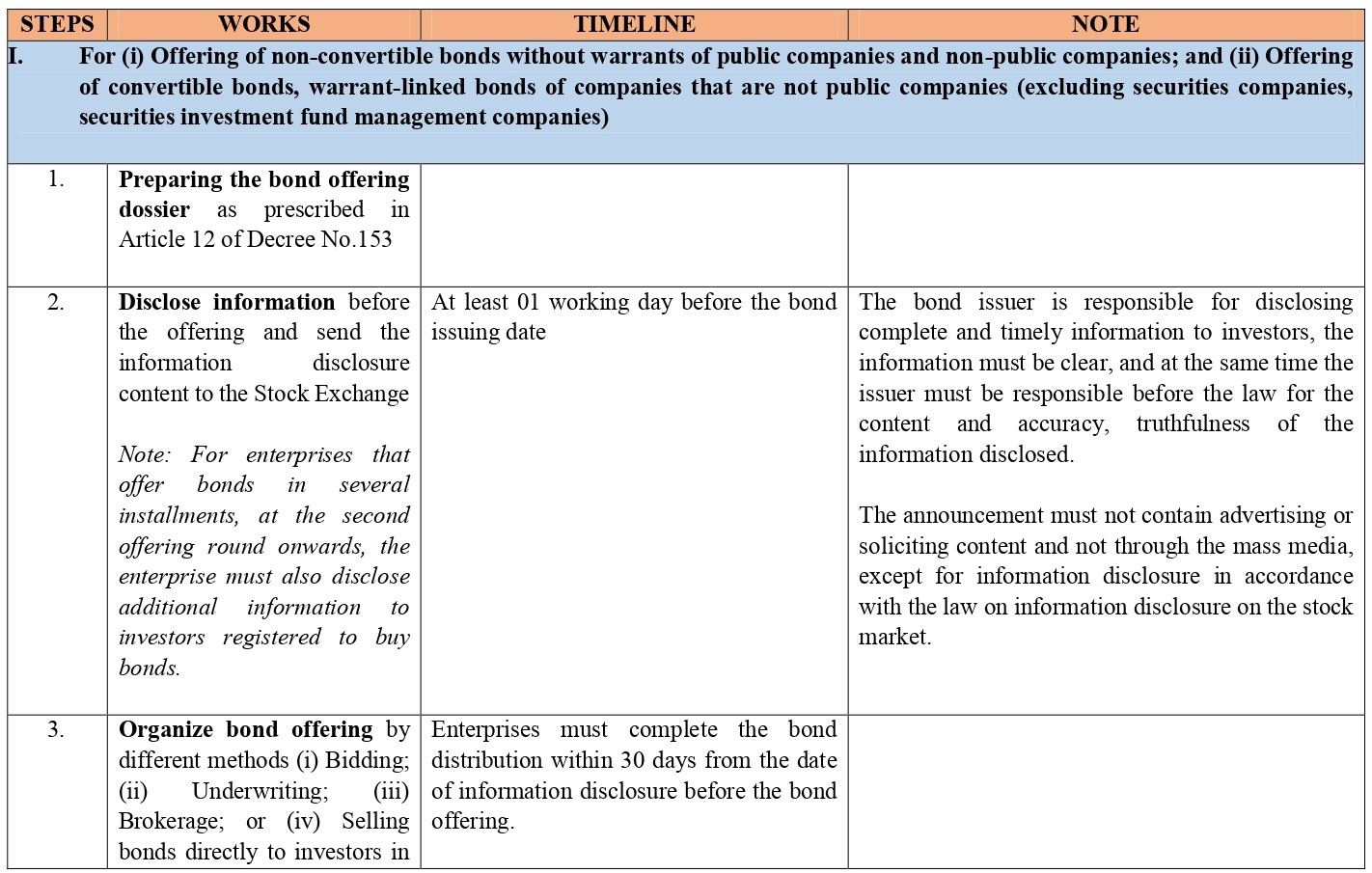

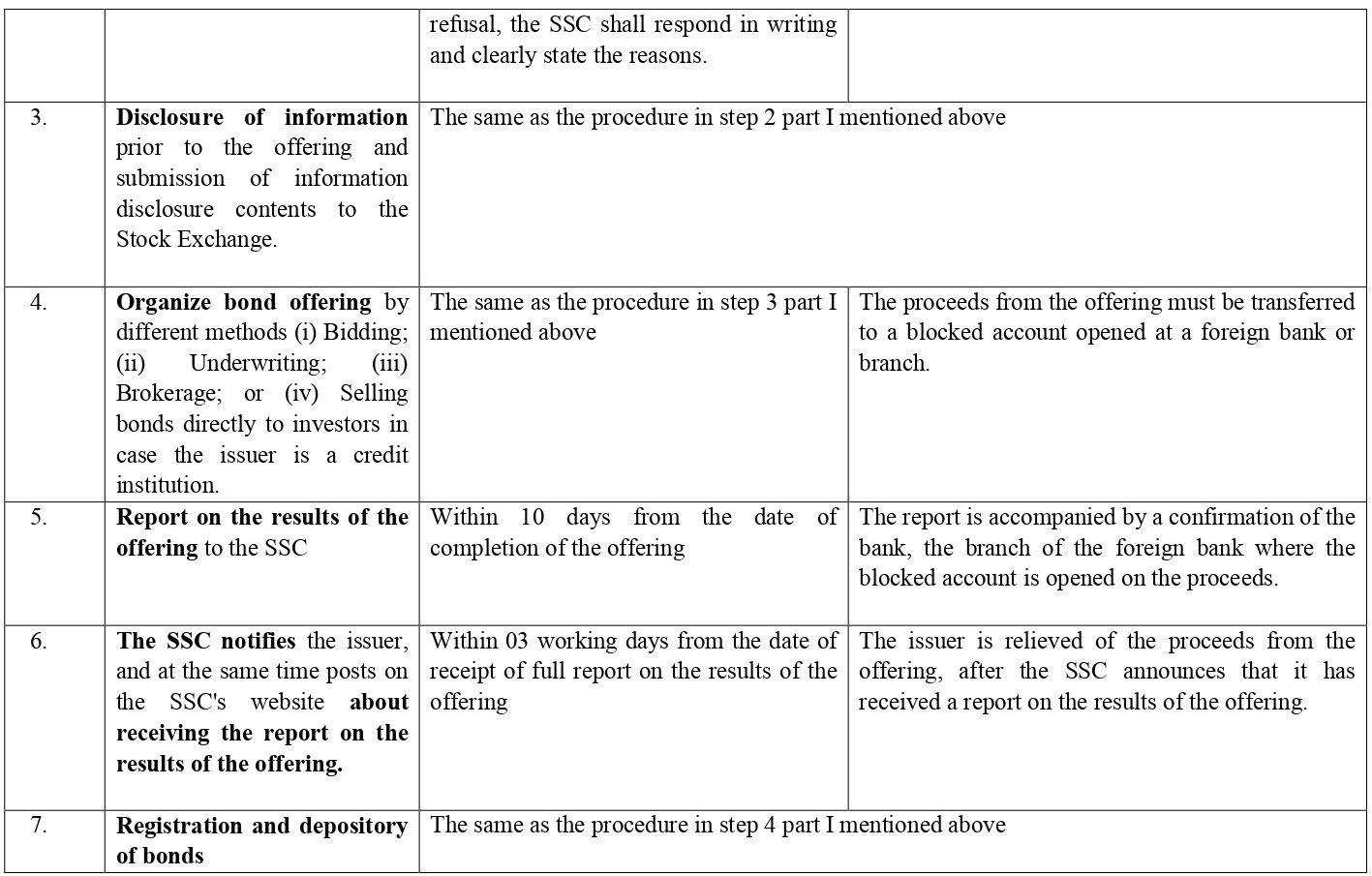

3. Procedures for private placement of corporate bonds in the domestic market

.jpg)

4. Further notes

After issuing corporate bonds, enterprises should pay attention to the following main issues:

a. For bonds issued in the domestic market, enterprises may only change the conditions and terms of bonds when (i) it is approved by the competent authority of the issuing enterprise; and (ii) it is approved by the number of bond holders representing 65% or more of the total outstanding bonds of the same type;

b. The issuing enterprise arranges sources of repayment of interest debts and bond principal from lawful capital sources of the enterprise and pays in full and on time to investors according to the terms and conditions of the bond;

c. Implement the disclosure regime including: (i) Disclosure of information about the results of the offering; (ii) Periodic disclosure of information; (iii) Disclosure of unusual information (if any); and Disclosure of information of enterprises on convertible bonds, bonds with warrants, early redemption of bonds, bond swaps, if any; and

d. According to the new regulations in Decree No. 65/2022, it is worth noting that enterprises must buy back bonds before the mandatory maturity when violating the issuance plan (including the capital use plan) or violating the law.

In general, after the scandals of Tan Hoang Minh[7]and Van Thinh Phat[8], the corporate bond market faces new challenges in a bid of state authorities and other stakeholders to make the market transparent, especially the sentiment and confidence of bond investors have been greatly affected. Hopefully, the bond market will witness positive changes in the coming time thanks to the management and regulatory efforts of the authorities, as well as the increased understanding and legal compliance of relevant entities to make this capital mobilization channel really effective in practice.

Note: The content presented above is for reference only. From time to time, the above content may no longer be relevant. For detailed advice, please contact DIMAC Law Firm.

[1] Article 4.17 of the Law on securities 2019

[2] Article 11.1 of the Law on securities 2019

[3] Article 9.1 of Decree 153/2020

[4] Article 9.2 of Decree 153/2020

[5] Article 9.3 Decree No. 153/2020

[6]Article 14 of Decree No. 153/2020

- Stock swap and its legal issues13/10/2020

- Legal update October 202013/10/2020

- Divestment – an inevitable matter in the M&A market02/10/2020

- 180-day probation term shall be applied to which employee?30/09/2020

- Legal update September 202028/09/2020

- Disputes Resolution for Investment under the EU - Vietnam Investment Protection Agreement (25/09/2020